Port congestion and drayage efficiency issues have re-emerged as significant challenges for North American container ports with the recovery of container traffic to previous peaks. Transport economist Phil Davies suggests that the current situation should spark renewed interest in potential solutions, including port terminal reservation systems, improved technology for coordination of container logistics, and the use of inland ports to transfer activity away from congested port terminals.

Total West Coast container traffic reached 24.7 million TEU’s in 2014, finally recovering to the peak levels achieved in 2006 and 2007. While West Coast container traffic Increased 3% in 2014, port, market shares were relatively stable in spite of labour issues, terminal congestion or port drayage questions that plagued West Coast ports in 2014.

All West Coast container ports with the exception of Prince Rupert experienced problems in 2014:

– All of the U.S. ports experienced major problems due to the standoff between the ILWU and Pacific Maritime Association over a new collective agreement. A new five-year agreement was finally reached in February 2015.

– The California ports of Los Angeles, Long Beach, and Oakland, experienced major port trucking issues related to container chassis logistics due to the divestiture of chassis fleets by the shipping lines.

– Port Metro Vancouver experienced a port trucking strike from February 26 to March 26.

– Seattle and Tacoma also experienced problems with intermodal rail service.

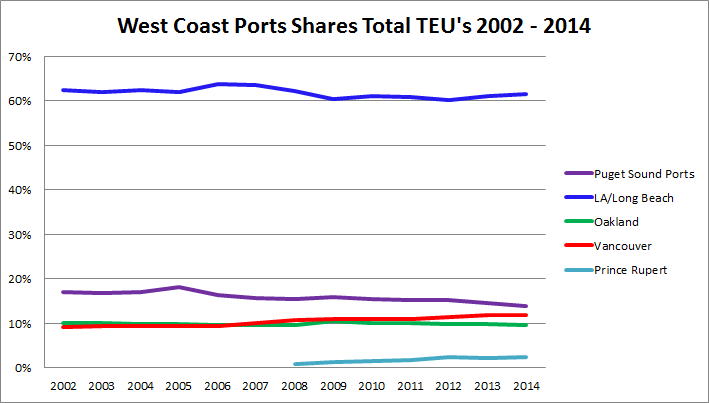

This turmoil had relatively little impact on container port market shares. The port of Prince Rupert appeared to benefit; their market share increased from 2.2% in 2013 to 2.5% for 2014. Vancouver was constant at 11.8%. The market share for LA/Long Beach increased from 61.0% to 61.4%, and Oakland declined from 9.8% to 9.7%. The Puget Sound ports of Seattle and Tacoma (now marketed jointly as the Seaport Alliance) saw their market share decline from 14.5% to 13.9%.

This turmoil had relatively little impact on container port market shares. The port of Prince Rupert appeared to benefit; their market share increased from 2.2% in 2013 to 2.5% for 2014. Vancouver was constant at 11.8%. The market share for LA/Long Beach increased from 61.0% to 61.4%, and Oakland declined from 9.8% to 9.7%. The Puget Sound ports of Seattle and Tacoma (now marketed jointly as the Seaport Alliance) saw their market share decline from 14.5% to 13.9%.

It remains to be seen whether the 2014 longshore labour issues on the U.S. Pacific coast will result in a permanent diversion of some portion of containerized cargo volume to different gateways. What is clear is that port trucking has emerged as a chronic problem at both East Coast and West Coast ports. Changes in industry practices have exasperated the situation. For example,

– The deployment of ever larger container vessels results in “bunching” of traffic at marine terminals. Resolution of terminal and road congestion problems is complicated by the reluctance of terminal operators to extend truck gate hours.

– For U.S. ports, changes in container chassis logistics have had a significant impact on drayage efficiency. Historically the shipping lines provided container chassis free of charge at U.S. ports. Starting with Maersk in 2009, the shipping lines have mostly stopped this practice and divested their chassis fleets to leasing companies. This has resulted in local chassis shortages and drayage inefficiency as truckers have to make additional trips to pick up or drop off chassis at container terminals or depots. Recent efforts to resolve these issues have focused on the creation of “gray’ chassis pools that allow truckers to pick up or drop off chassis at multiple terminals, though the long-term impacts of this solution are still unfolding.

The above examples suggest container market share growth will go to those entities that apply new approaches and solutions to solve the port congestion and drayage efficiency issues. Such actions (along with timely logistics infrastructure investments) are needed to support the growth in container trade volume required by shippers.